Germany experienced little increase in unemployment during the Great Recession, and has found “internal devaluation” relatively easy and pain-free, unlike most other countries. Why ? Some observations on the role of social capital in financial crises.

Theoretically, a drop in general demand in the economy would not necessarily have to result in unemployment, if businesses were willing or able to reduce their costs by cutting everyone’s pay, rather than sacking a part of the workforce. An alternative to a general pay cut would be to reduce everyone’s work hours, which still result in lower incomes for individual workers. But in the real world, neither scenario happens because:

- firms don’t want to demoralise their entire work force by cutting everyone’s pay, rather than quickly firing a large minority of the workforce they won’t ever see again ; and/or

- unions and/or labour regulations may constrain businesses from acting in this way, especially for lower-skilled workers ; and/or

- firms may want to keep the best workers and get rid of the worst, and a general pay cut will encourage the best to leave even in a recession.

Even if there is unemployment, wages do not fall quickly in response to the excess supply of workers (nominal wages are ‘sticky’) for many reasons, one of which is that a mismatch between old and new jobs may persist in the economy. It takes time for unemployed programmers and bankers to retrain as lawyers and master-carpenters, or adjust expectations downward and become cooks and taxi drivers. So waiting for wages to come down in order to clear the labour market or get rid of unemployment is a painful process. Government policies can shorten or prolong it, but one way or another it almost always takes longer than anyone wants.

The point is, if the adjustment in a recession could take place primarily through a proportionate reduction in everyone’s incomes, rather than through the unemployment of a large minority, the pain of recession could be widely shared rather than concentrated and the recession itself might also be shortened. But basically that ‘pain-sharing’ never happens, because it cannot. There’s a coordination failure in the economy as a whole.

If you have high unemployment and a budget deficit, you need to borrow that fiscal shortfall from the bond market, or the IMF, or a generous benefactor. But if you can’t borrow or there are limits to borrowing, then you must cut back on spending or raise taxes (i.e., austerity) and make everything worse. A country which controls its own currency can devalue it and create a trade surplus, which can soften the blow of austerity (at least as long as your trade competitors don’t return the favour with a devaluation of its own).

But if you cannot conduct a sovereign monetary policy, then all your adjustment must be internal, i.e., as Andrew Mellon allegedly advised Herbert Hoover, “liquidate labor, liquidate stocks, liquidate farmers, liquidate real estate… it will purge the rottenness out of the system. High costs of living and high living will come down… Values will be adjusted, and enterprising people will pick up from less competent people…” Mellon was colourfully arguing for “internal devaluation”, i.e., essentially the same idea as a fire sale in a buyer’s market with an unsold inventory of cars or a glut of new houses.

But “internal devaluation” is prolonged and painful. The primary and fastest lever of alleviating recessions — monetary policy — is disabled by things like the gold standard of the 19th century, or the euro of today. The pain of adjustment-through-recession might be alleviated, even avoided, if everyone could “share the pain”, rather than a select group of people be unemployed. But that just does not happen, because it cannot — except in Germany.

§ § §

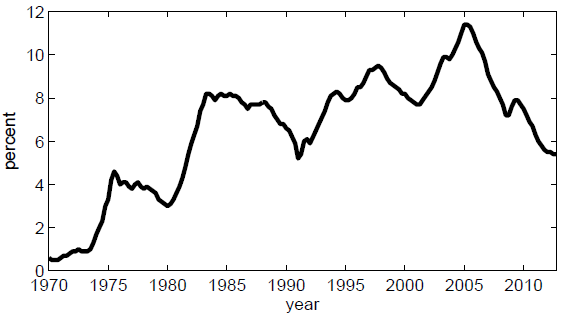

It’s easy to forget now, but in the mid to late 1990s, Germany was derided along with France as one of the sick men of Europe. While the United States elated in economic triumphalism as its unemployment rate reached a historic low of 3.9%, the rates in the ‘big’ economies of Western Europe were mired in the 10-12% range, with Spain at even higher levels. And most of these economies were not in recession. As a cure for Eurosclerosis many argued for the implementation of Thatcher-like restructuring, with big tax cuts, big reductions in state spending, deregulation, and retrenchment of the welfare state.

In the case of Germany, following reunification it spent hundreds of billions of Deutschmarks to boost the eastern states — along the lines of 4% of West German GDP annually between 1991 and 1999. [source] This did not fully close the gulf between east and west, but German costs did rise, competitiveness was eroded, and Germany’s structural unemployment remained high.

Some time in the late 1990s, something changed within the German economy, and it was definitely a supply-side event, i.e., Germany’s labour costs began to fall relative to its trading partners’. Here’s an international comparison of unit labour costs, or wages relative to productivity [source], with 1995=100 :

For a high-wage country like Germany which had been reputed for labour rigidity, that’s a pretty steep rise in international competitiveness ! Germany accomplished an internal devaluation, which eventually paid off in a reduction of the unemployment rate :

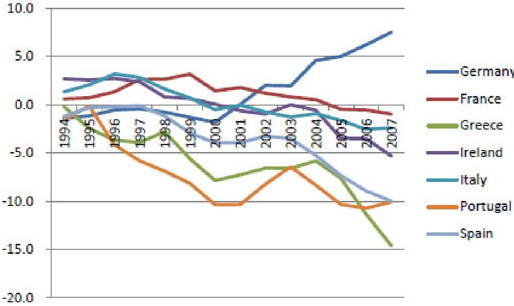

as well as a big rise in Germany’s external surplus [in % of GDP, source : S. Wren-Lewis] :

These effects are often attributed to a series of reforms collectively known as the Hartz plan implemented between 2003 and 2005. They were a mixed bag of legislations enabling low-wage “mini-jobs“, curbing early retirement options and (most controversially, in Hartz IV) reducing long-term unemployment benefits. The Hartz reforms must have done something to reduce structural unemployment, especially for younger and older workers, if only by reducing unemployment benefits. That seems a reasonable interpretation, but it is in fact disputed by many people (e.g., 1, 2, 3).

Since at least half the improvement in German competitiveness predates those reforms by nearly 10 years, there must be other important reasons.

§ § §

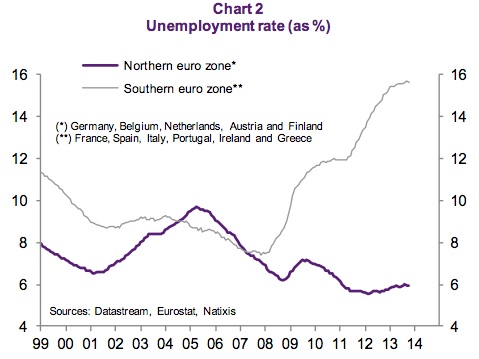

Even more interesting is that Germany’s recession in 2008-9 was quite shallow in terms of unemployment, i.e., the pain was “widely shared”. Although GDP contracted more in Germany than the USA or France,

the German unemployment rate barely blinked [both charts from here] :

But why ? In the 2008-9 recession, in response to falling orders, German firms reduced labour utilisation by cutting back work hours rather than by laying off workers. In fact, a whopping 90% of the drop in total labour inputs in the German economy in the Great Recession is to be explained by reduction of hours per worker ! This kind of “labour hoarding” does not normally happen during recessions in other countries, but did happen in Germany this time. This mini-miracle now has people on the centre-left all over the world seeking ways to replicate it in other countries, and has spawned a substantial literature.

In Germany, firms face restrictions on sacking workers in the first place, but in case of economic difficulties, they can apply to the Federal Employment Agency (Bundesagentur für Arbeit) for “short time” or Kurzarbeit. (Not the same as the 35-hour work week made famous by France, which is a statutory definition of full-time work.) The application entails a protocol for reducing work hours per worker, with the request triggering a process of consultations between the BA, management and works councils inside firms. After an agreement, workers can receive unemployment compensation in proportion to the loss in working hours. (There are great many more details, but they are really boring.)

There are sceptics who argue the effect of the Kurzarbeit system is exaggerated and the muted response of the German labour market to the Great Recession was due to the wage restraint of 1999-2008. Also, there had been a shortage of skilled labour which German manufacturers would not want to lose even in a recession. There’s some reason to think this is at least partially correct. Parts of the Kurzarbeit system go back as early as the late 19th century. In previous recessions, German firms had actually always resorted to hours-reduction more than in other countries. For example, during past recessions in the USA, ~30% of the reduction in labour inputs has been “intensive”, via adjustment of hours, whereas in Germany it has been ~60%. (source)

§ § §

An explanation which best accounts for the dramatic rise in Germany’s competitiveness after the mid-1990s, that’s also consistent with its amazing labour market flexibility during the Great Recession, is contained in Dustmann et al. (2014). The argument hinges on a major institutional characteristic of Germany’s. Since it’s impossible to describe an industrial governance structure with charts or data, I simply quote from them [emphases mine]:

…the specific governance structure of the German system of industrial relations offers various margins of flexibility. In the early to mid 1990s, these institutions allowed for an unprecedented increase in the decentralization (localization) of the process that sets wages, hours, and other aspects of working conditions, from the industry- and region-wide level to the level of the single firm or even the single worker, which in particular helped to bring down wages at the lower end of the wage distribution. This decentralization took place even though the institutional setup of the dominating system of industry-wide wage bargaining basically remained unchanged.

The specific feature which we stress here is that the governance structure of the German system of industrial relations is not rooted in legislation and is not governed by the political process, but instead is laid out in contracts and mutual agreements between the three main labor market parties: trade unions, employer associations, and works councils (the worker representatives who are typically present in medium-sized and large fifirms).7 For this reason, Germany was in the position to react in an unprecedented way to the challenges of the early 1990s.

[7] Works councils have to be set up in establishments with more than five employees when demanded so by the employees. About 92 percent of employees in establishments that have more than 50 employees work in establishments with a works council, but only 18 percent of employees in establishments that are smaller…

The principle of autonomy of wage bargaining is laid down in the German constitution and implies that negotiations take place without the government directly exerting influence. As such, Germany has had no statutory minimum wage imposed by the political process over the period we study. Rather, an elaborate system of wage floors is negotiated periodically between trade unions and employer associations, typically at the industry and regional level.

…As a consequence, negotiations are usually far more consensus-based and less confrontational than in other countries. For example, Germany lost on average 11 days of work each year per 1,000 employees by strikes and lock-outs between 1991 and 1999, but only five days per 1,000 employees between 2000 and 2007. These figures for the earlier and later time period compare to 40 and 32 days per 1,000 employees in the United States, 30 and 30 days in the United Kingdom, 73 and 103 days in France, 158 and 93 days in Italy, and 220 and 164 days in Canada…

In Germany, contractual agreements between unions and employer associations are negotiated either on the region-industry level or on the firm level. In addition to wages, working time regulations are an important component of the negotiations.

A distinguishing feature from US labor market institutions is that the recognition of trade unions in Germany is at the discretion of the firm, and union contracts cover only the workers in firms that recognize the relevant sectoral wage bargaining (union) contract—regardless of whether the worker is a union member…

Also, German firms that once recognized the union contracts can later opt out at their own discretion. Even within union wage contracts negotiated at the industry level, there is scope for wage flexibility at the firm level through so-called “opening” or “hardship” clauses, provided that workers’ representatives agree…

After opting out of a collective agreement, firms still have to pay wages for the incumbent employees according to the collective agreement until a new agreement at the firm level has been reached, but they do not have to honor new negotiated wage increases and the firm need not follow the old collective agreements for new hires. Thus, over time a firm may be able to lower wage costs considerably by opting out of the union contract—provided its employees accepted this.

[ The Economist also had a really readable piece on a similar theme, an intimate portrait of how worker-management relations work inside a German company to maintain both quality and competitiveness. ]

Within a minimal institutional framework set up by statute, it is left up to workers and management to work things out themselves. Dustman et al.’s argument is equivalent to saying, Germany’s wage restraint [relative to productivity growth] since the 1990s was a natural, ‘market’ outcome of negotiations between management and labour in response to the erosion of competitiveness after German reunification. (Of course, it did help with the employers’ bargaining position with workers that part of their production could now be offshored to Eastern Europe after 1989.)

Most European countries have copied aspects of the “social partnership” model of ‘codetermination’ between government, business, and labour which in Germany is known as Betriebsverfassungsgesetz. But imitation has not produced similar results, and some countries have a more decentralised system of ‘co-determination’ than others. In France and some Mediterranean countries, the state frequently intervenes in the bargaining between business and labour, because (I would argue) there’s a much more adversarial relationship between labour and business. Contrast with the Anglosphere — it also has an adversarial relationship between business and labour, but then it has relatively few labour protections/regulations and basically no coordination of bargaining.

To simplify a little bit, the Anglosphere has social conflict and the state intervenes relatively little in the bargaining process; but in France and the Mediterranean, there is more social conflict and there is more state intervention. In Emmanuel Todd‘s scheme, the Anglosphere is individualistic and non-egalitarian, but France is individualistic and egalitarian. In the latter, the state must arbitrate and ‘fix’ things.

§ § §

The relatively decentralised labour market institutions of Germany and the other northern countries reflect their lower level of social conflict. Germany, Austria, Switzerland, Denmark, Norway, Sweden, and Finland are well known for their efficient labour markets despite what, from an Anglo-Saxon perspective, should look like rigidities. And these same countries also do not have statutory minimum wage laws but still manage to have the de facto equivalent — wage floors set by bargaining between workers and management.

[The Netherlands, with its “Polder model“, also belongs in the list of decentralised bargaining countries, but it does have a minimum wage law. By the way, Germany has just recently passed a minimum wage law.]

Is it a coincidence that the northern Eurozone had a curiously parallel experience of the Great Recession (source) ?

Initially, the northern Eurozone countries experienced a similar, or deeper, crash in GDP than the southern countries ; yet their unemployment rates barely moved. [In the above, France is included in the “southern economies” even though it’s really intermediate between the two. So the southern economies actually look worse if France is excluded.]

So can this system be duplicated elsewhere ? I say no. In the Anglosphere it requires too many constraints on business than is currently regarded as politically and culturally palatable. In Europe outside the northern economies the constraints are regarded as too few ! The decentralised system of ‘co-determination’ is likely something that can only exist in societies with a lot of social capital, i.e., those which are cooperative, consensus-prone, and high-trust.

That social capital also shows up in the political system. A Swedish blogger who specialises in personality psychology explains how a “feminine personality” manifests itself in a “consensus democracy” :

The other main aspect of femininity, cooperation, is something that is found in the political systems of these countries. The Feminine region is characterized by consensus democracy, especially in the sense that these countries have proportional electoral system, lots of political parties that form coalitions and with the ambition of getting broad support for decisions, not just within coalitions but with opposition and other interest groups and institutions. It’s the friendly, inclusive, and cooperative way of governing.

In contrast, the Anglosphere is characterized by the majoritarian model (see the link above) in which countries have fewer parties, form less coalitions with often just a single party in government at a time. The government also focuses more on their own agenda with less concern for and compromise with other parties, interest groups etc. It’s the competitive and take-charge way of governing.

Calling it ‘majoritarian’ actually understates the winner-take-all approach of the competitive model in the Anglosphere. Not a single government in the UK has received a majority of the popular vote since before the war, and the last time one came even within the upper 40s was in the 1950s. Yet, because of a combination of single-branch government and first-past-the-post voting, a plurality party in the UK can attain power and not necessarily achieve consensus in society even when implementing fairly radical legislation (e.g., Thatcher, who never got more than 42-43% of the vote).

In France, Thatcher would have been impossible simply because of the absolute-majority voting system. But even if a Thatcherite came to power with >50%, there would have been blood in the street from the minority out of power ! Of course the first few years of Thatcherism also provoked unrest in the UK, but one imagines it would be far worse in France with its long history of labour agitation and at-the-drop-of-a-hat demos.

§ § §

Within the Eurozone, Germany’s current account surpluses have been a problem, which even the IMF and the US Treasury have criticised. But these surpluses were caused by internal devaluation — something almost nobody ever does voluntarily or accomplishes without pain. Germany’s labour market reforms, especially Hartz IV, are unpopular and, by German standards, pretty divisive. But they took place without massive social cost and without an extraordinary, compelling urgency, such as an external debt or a balance of payments crisis. I just can’t imagine something comparable taking place in France without triggering unrest even with a major emergency.

The ultimate cause of Germany’s problematic strength in the Eurozone is not an authoritarian culture, or primordial savings behaviour, or economic unilateralism, but its amazing institutional capacity and social capital. Surely that is as impressive as any feat of German engineering, or as exceptional as the logistical efficiency with which Germans of the past waged two-front wars.

Your thesis is persuasive as far as an explanation for Germany’s employment-rate/unit-labor-cost behavior, but we end up with a similar question just a level deeper. Instead of “what about germany leads to high-employment/low-unit-labor-cost” the question becomes “what about germany leads to quality labor institutions”. More narrowly, why do german workers cooperate with a system that’s restraining their wages? They’re clearly willing to sacrifice for their firms, their labor institutions and the German unemployed/potentially-unemployed. Some combination of nationalism and cooperation-with-authority doesn’t seem far-fetched, or at least worthy of further investigation.

Further, does low unit-labor-cost necessarily lead to current account surpluses, debt crises, and internal devaluations? Policy could have encouraged the corporate margins justifying all that German employment to be consumed or invested domestically, or the foreign-investment-bound euros to buy real or private assets instead of nominal public assets. Euro fiscal or monetary policy could reflect the whole rather than German interests. Do you really think our analysis of Germany’s motivations should change much whether the low-labor-costs are the results of labor institutions or public policy? Your point is excellent but doesn’t seem to actually conflict much with Todd’s analysis.

I really enjoy your writing.

LikeLike

Pingback: Der Todd des Euro | Pseudoerasmus

“what about germany leads to quality labor institutions”

Well I don’t state it explicitly only because I assume if you’ve read other comments and posts of mine you know what I mean when I use phrases like “human capital” or “social capital” or “high trust” or even “culture”.

Todd’s idea of culture is an old-fashioned, dated one where behavioural traits persist for no particular reason. Some mediaeval archetype of the German family circa 1000 somehow gets reflected in the social market economy.

“does low unit-labor-cost necessarily lead to current account surpluses, debt crises, and internal devaluations?”

Currency devaluation, if it results in a trade surplus, implies you are “exporting” unemployment to your trading partners. Sometimes your partners engage in competitive devaluation to counteract it.

But I’ve never heard of competitive internal devaluations ! At least not deliberate ones

LikeLike

This is interesting — more interesting to me, perhaps, because I am smack dab in the middle of The Great Rebalancing right now. Just finished his section on China and have not got to the second half where he focuses on the Eurozone.

When I am finished with that book (probably some time next week) I will come back and reread this post and offer a few more substantive comments then.

But a solid post.

P.S. Have you ever heard of Mary O’Sullivan’s Contests for Corporate Control: Corporate Governance and Economic Performance in the United States and Germany ? It has been on my to read list ever since I read found it in the foot notes of Karen Ho’s Liquidated:. It seems relevant here.

LikeLike

I should look at it but it sounds really dull ! ( When ever the word “governance” is used the bell usually thuds not tolls.)

Just to clarify, the above was not really a “take” on the Eurozone crisis, or a view of how the problems associated with the euro might be solved. To be honest I’m no longer all that interested in current events and policies. Rather this post was my alternate “anthropology” of the Germans and how that manifested itself in economic behaviour.

LikeLike

Myb6 — Near the end of the post I suggested this was not just about Germany, but something common to all the continental northern European economies. I did not elaborate because (1) the post was already pretty long ; and (2) I know Germany and its business governance structure pretty well but the other countries I would have to swot up on and, mercy, are labour-business governance issues dull !

LikeLike

Trust makes it easier for two parties to come to an mutually-beneficial agreement; I’m asking why employed German workers, the vast majority of whom would not face unemployment, even perceive the low-wage deal as beneficial to them in the first place.

“Internal devaluations” purely because of the eurozone context, as discussed in your post. I’m asking whether there were alternatives where Germany kept its unemployment low without creating economic problems for its neighbors. If so, then it’s right for a Frenchman to ask why Germany did not choose such alternatives, and adjust their views of Franco-German relations accordingly.

Putting it together: German society had a preference for the low-wage deal (why? TBD), was able to execute that preference due to high-trust/institutional quality (Pseudo, 2014), then- maybe, open to evidence otherwise- allowed that policy to harm their neighbors through inaction and active impediment (why? TBD). Couldn’t Todd’s analysis be a factor in the two remaining “TBDs”?

Thanks again for your writing.

LikeLike

no no no. german workers did not choose a low wage option, unit labour costs falling does not necessarily mean wages are falling, just means wages not rising as fast as productivity, what happened in germany 1995-2005 was wage restraint esp relative to other euro economies. and the interesting part of the story is that this happened in a unionised context but still working like a freeish labour market, normally unions make labour markets inflexible… i just don’t understand how that can be described as some chauvinistic-nationalist policy of dominating neighbours.

what might have been done before the crisis ? well nobody forced greece and portugal to expand government debt so much while their economies were growing, ireland and spain were running budget surpluses but their private sectors were borrowing huge sums for real estate speculation and that’s difficult to identify as a problem in real time. what could germany have done different that was also reasonable ? i really don’t know. the ecb might have curbed bank lending to these countries, but the fed might have done the same with capital ratios & so on in the usa and they did not, so how can you cast stones. but that’s the past. you can make a case that since the crisis germany has not been acting as a european multilateralist, it’s been acting like a selfish country — but a normal selfish country. germany could have dropped the insistence for “conditionality” as part of the bailout package but what normal country spits out hundreds of billions of € just like that without any strings to foreign countries. now for me the stupidity is bailout countries (spain, portugal, greece, ireland) didn’t use the threat of default to get better terms out of germany (and france), both their countries’ banks are heavily exposed.

sorry for disorderly sentences i’m posting from my mobile since i lack access to a computer at the moment.

LikeLike

No worries about the disorder, it’s remarkable (and appreciated) that you’re even responding on your vacation!

Wages haven’t fallen, but German workers chose a deal whereby wages in Germany were lower than they would have been otherwise, thus achieving a more competitive unit-labor-cost. That’s an opportunity cost to the workers. Why’d they take that deal?

The US didn’t restrain bank lending but the US is feeling the pain. The German-dominated ECB didn’t restrain lending but expects the South to feel the pain. But I don’t want to shift to PIIGS/lending, despite the obvious relevance, because both Todd and your post were talking more about France/Germany and trade competitiveness. Imbalances were a political issue before the Great Recession, Germany could have shifted taxes from consumption to income/corporate &/or increased government consumption. Today Germany could do those things and support a European, not German, ECB policy (ie looser).

Multilateralist vs normal selfish country is the crux of the issue. If Germany is a normal selfish country, other Europeans would be pretty stupid to further integrate. If German institutions are higher-quality and thus more capable of enacting the German (normally selfish) will, that actually makes the problem worse.

Haha, I actually hope you ignore my reply for a little while and enjoy your time off.

LikeLike

it’s not that german workers rolled over and exposed their bellies, as i mentioned in the post the bargaining position of german firms improved when eastern europe was opened up for their investment, the interesting thing about germany is that almost seamlessly without political intervention or labour unrest wage-bargaining shifted from the level of trades unions to within-firm works councils, in france and southern europe union wages are negotiated at the national level and german like decentralisation would not be possible because either the unions’ national hierarchy would get involved or the government would step in and decentralisation might require legislation. yet this same decentralised system for germany had produced a high level of job protection and wage growth for workers during the postwar boom. i think germans (as well as japanese) are depicted as authoritarian and deferential to hierarchy because of their past but i think of them as societies based on trust, consensus and cooperation. no one has any problem with that description if it was about norway or denmark presumably because they have been too small to cause any of their neighbours problems in the past. but imo the same social force that has traditionally allowed german municipal subway systems to operate on an honour system, also permits the same decentralised industrial relations. (yes, yes, yes, today there are now many more u-bahn inspectors with their random checks than there used to be in the past, just like Japan’s paternalistic “life-time unemployment” is slowly fading away.)

LikeLike

https://pseudoerasmus.com/2014/08/01/todd-on-the-euro/comment-page-1/#comment-937

LikeLike

Hi Pseudo,

You are convincing on the quality of decentralized German labor institutions, however could you clarify what German workers saw to their benefit in the low-unit-labor-cost deal? Labor institutions may be less-flexible and -adaptive in other countries, but I doubt other countries’ laborers would take the German deal at all. Trust/Cooperation is not an answer here: in your example, it reduces the transaction costs between transit-riders and transit-providers, but Trust/Cooperation by itself does not explain why transit-riders want to ride the transit. In the transit case the mutual benefit of the deal to the involved parties is obvious; not so in the low-unit-labor-cost case.

Authoritarian/Deferential vs Trust/Cooperation: could you detail why you believe the latter is more accurate? The results could look similar in macro outcomes. Also, if internal trust/cooperation leads to external predation, the distinction is irrelevant to France anyways: whether the behavior has positive- or negative-mood descriptors, France would still be stupid to integrate. German self-sacrifice, whether due to obedience or cooperation, seems to stop at the border and that should inform French decision-making.

Many characteristics hold across the Low Countries, the Alps, Germany, and Scandinavia. But the eastern border of the macro-region (Elbe/Prussia, pre-war Austria) clearly has a relatively more imperial/expansionist history and that could have genetic or cultural consequences still relevant. If Germany=more-populous-Scandinavia is your argument, it’s something you might want to flesh out further in future posts.

A fascinating discussion.

LikeLike

I’ll add that in my comments I’ve been focusing more on nationalism/authority/whatever-you’d-like-to-label-it and haven’t even mentioned stem families, because yes Todd is over-selling stem families as an explanation for that trait.

LikeLike

(1) from a self-interest perspective i assume it’s because german workers understood that it was in the long term interest of their own employment if the competitive position of their firms improved, i guess what i’m saying is that social trust can overcome the coordination failure that inheres in adversarial relationships. or maybe it’s not that at all, maybe there is a collectivist impulse, similar to the way japanese corporations, traditionally anyway, reassigned workers internally rather than lay them off, except in the german case it’s the workers that agreed to wage restraint. but of course that system in japan is being eroded as we speak.

(2) where is the “external predation” ? france may have been stupid to integrate, but surely not as stupid as greece or portugal. i find the current french situation very similar to the late 1990s when the franc was shadowing the dm even as germany maintained high interest rates as part of emu and france stuck it out even though it had high unemployment. it could probably do the same now.

(3) german self-sacrifice stops at the border… you do realise it’s the combination of france AND germany which have required austerity from greece et al ? france and germany are both seriously exposed to the debt of the eurozone economies.

(4) german imperialist-expansionist history…what about french imperialist-expanionist history ??? liberal traditions in western germany are as strong as france’s, the western german cities had a very festive-riotous 1848, especially baden, rhineland-palatinate and the old free cities. but german unification was accomplished by prussia which had more backward traditions. i have a blog post in the works about whether the soviet truncation of DDR helped liberal consolidation in the BRD (as we used to say)

(5) many people argue the ecb is now no longer inflation targetting it is “deflation targetting”, which would be a very amusing phrase if it wasn’t so tragic… by the way in the vein of “statistical elves can ruin our lives”… google “potential output revisions” and “cohen-setten”…

LikeLike

(1) We’re communicating well on this point now.

(2) The predation is about trade balance and pre-dates the Euro, and yeah Greece/Portugal is in a much worse position than France.

(3) Todd’s point doesn’t require a saintly France, though the creditors of France should feel their share of pain. But it’s hard to hold France to account for the trade imbalances which underlie the crisis, or Germany’s resistance to looser monetary policy at the ECB or a domestic shift from saving to consumption/investment, either of which would help France and the PIIGS.

(4) I think we’re agreeing here: the cultural traits that Todd considers threatening exhibit a cline towards the eastern marches of the Germanic sphere, and those marches don’t group with Scandinavians, nor with the French. Whether or not there’s really a major trait discontinuity at the Rhine, we’d need to get data at the regional, not national level. This I would consider a fair criticism of Todd- he’s using his finely-grained family systems data to explain very coarse-grained macroeconomic trends.

(5) It seems counter-productive to be so sneaky about targeting, given that to reach those very targets the ECB needs to shift market expectations!

LikeLike

so is our only disagreement now semantic, about the word ‘predation’ ? the euro and non-euro countries that ran current account surpluses in the 2000s are : norway, sweden, finland, denmark, austria, switzerland, the netherlands, belgium and germany. of course germany matters most but during the last decade it was a general tendency in the northern half. also the northern euro countries de facto devalued their currencies by joining the euro.

i think the ecb’s resistance to looser money is now institutional, goes beyond germany. i don’t see how expenditure-switching will help in the short to medium term since that will take forever ! germany has already passed a minimum wage law and it won’t take effect for until some time next year.

LikeLike

If you’re saying the current account surpluses are the result of a general N European cultural trait, I’m open to that argument, and a post expanding your labor-institutions argument to other northern countries would be awesome. But I’m agreeing that the origin of the current account surplus need not be considered predatory, but rather the response. The political pressure to adjust was on Germany*, and the response was schadenfreude. It only got worse after the euro crisis clarified the harm to the deficit countries. It’s impossible to know for sure whether the other Northern countries would react the same way in Germany’s position; if you think so I’d listen to your case.

*: Belgium/Denmark/Finland/Austria haven’t been consistently large surplus though the Danes are becoming so, Norway/Switzerland/Sweden aren’t euro so adjustment could be currency-based (Denmark too, ish: ERM etc), Germany is 5X the Netherlands. Politically, surplus is almost entirely a German problem.

It’s questionable to separate the ECB’s institutional stance against inflation from German culture and public opinion. Expenditure-switching is exactly what Germany is insisting upon from the deficit countries.

We’re in general agreement, we just differ on the degree which your ideas, as presented thus far, conflict with Todd’s cultural thesis.

LikeLike

You say Todd and I are not far off, but I think we are since I stress things like national variations in social capital, time preference, productivity, etc. rather than some unusual degree of selfishness on the part of one country.

The case for Germany being unusually selfish or predatory is weak, even if you considered just the response to the crisis.

Germany because of its size matters most, but its general unwillingness to dole out money — with or without conditionality — is simply natural. Paying for the bailouts of foreigners is not popular anywhere in the Eurozone.

I’m all for expenditure-switching by Germany but imagine asking a country to run budget deficits of 3-4% of GDP on behalf of foreigners !

Sure you can’t separate German preferences from ECB policy, but there’s been a north-south split in the ECB governing council for several years now.

The problem is normal nationalism — one of nation-states caring more for their own than for foreigners. That’s not a new observation by any means, but as Craig Willy suggests in passing the general reluctance for redistribution across borders is mirrored by the general reluctance for redistribution within countries which are heterogeneous. I put in a comment over there which is still awaiting moderation, and it contains a link to ( http://www.nber.org/papers/w8524.pdf ) Its abstract has unnecessarily invidious verbiage, but the general thrust of the paper (and many others along the same lines) is that heterogeneity is negatively associated with income redistribution in general. People are more willing to share with others like themselves.

LikeLike

Other bailout examples do not parallel (where else is the employment situation so dire, the creditors so likewise-responsible, benefiting so much, or blocking adjustment?), expenditure- and tax-shifting is not the same as a deficit, any argument against a German deficit applies to the structural surpluses proposed for the PIIGS, monetary policy could be Zone-appropriate instead of German.

Anyways, we’re beginning to circle, and I’m merely proposing a somewhat-narrower conclusion until you’ve strengthened the other links in the chain.

LikeLike

i’m not sure what we are disagreeing about because on the sheerly macro issues i agree completely. germany could shoulder most of the burden of adjustment.

LikeLike

A very dense blog post and discussion. I like Todd’s thesis. It has a certain explicative power, but of course doesn’t explain everything (no one factor ever does). I like most of your socio-anthropological additional explanations.

Accounting for the superiority of the German economy is a fascinating subject. The comparison with France leads to a lot of soul-searching, but often focuses on the wrong questions.

You mentioned discount rates in the first part : I believe that this ties into the family-structure model.

1) German enterprises have long-term orientations (and are significantly more family-owned than comparable French companies).

2) French capitalists are stupid, always concerned with short-term gain, with very little concern for their workers, the communities they exist in, or the wider environment. This is true in the long term : 19th century French capitalism emphasised speculation over productive investment.

3) German workers have greater respect for hierarchy and authority, and are ready to dialogue with employers, who have a certain paternalistic respect for them

4) French workers are independent-minded and suspicious of employers in negotiation, and rightly so (see 2)

5) Germany has an education and training system which is closely geared to a high-added-value economy. Any country can produce good engineers, but good technicians and tradesmen is actually much harder, and Germany does it well

6) France is still struggling with an ossified education system geared to the needs of producing the intellectual elite for a previous century, massified to teach irrelevant stuff to kids who should be in apprenticeship

What concerns me is that the virtuous Germany is demanding that the sluggard economies toe the line, holding itself up as a paragon of virtue, but emphasising elements that have absolutely nothing to do with Germany’s advantages, and will not help other economies catch up.

On similar themes, you may be interested in my review of Wolfgang Streeck’s newly translated book :

European Tribune – Community, Politics & Progress.

LikeLike

Pingback: ¿Qué es soberanía? Salvar a Europa de los europeístas | Club Pobrelberg

Pingback: Where do pro-social institutions come from? | Pseudoerasmus

Very late, but I point this nonetheless. You said in the comment you did not want to lengthen the post (and your own time spent to learn it) by considering the different “Arbeitsgesetze” but without being a specialist my self, the”cassa integrazione” in Italy could be a enlightning comparative to the Kurzarbeit. It is old, was much used since the seventies, but has some slight different mechanisms (mainly size of companies involved, governement involvment I would tentatively say).

Anf the unemployement story is very different in both countries.

LikeLike

Pingback: Thursday assorted links - Marginal REVOLUTION

After the 2010 general election the Conservative-Lib Dem coalition government was formed, which had received a majority of the popular vote.

LikeLike

Got here from the MR re-post a couple weeks ago, but any historical/cultural theories on why Germany has better developed social trust/lower social conflict? I’ve lived in the UK, US, and Germany and your hypothesis definitely feels right to me anecdotally.

LikeLike

Pingback: Where Do Pro-Social Institutions Come From? - Evonomics

Pingback: Are Bosses Dictators? | book r7ty

Pingback: Are Bosses Dictators? | The New Yorker - Evanino.com

Pingback: Are Bosses Dictators?

Pingback: Labour repression & the Indo-Japanese divergence | pseudoerasmus

Pingback: Where Do Pro-Social Institutions Come From? - Evonomics

Pingback: ¿De donde vienen las instituciones prosociales? - Almacén de Derecho

Pingback: Reading notes (2021, week 22): On better metaphors, employers ruling our lives, the math on social security, and efficiency being overrated – Richard Brisebois PhD